What Are My Mortgage Options? (FHA Guide to Partial Claims, Loan Modifications & Selling Your Home)

May 01, 2026

📝 What Are My Mortgage Options? (FHA Guide to Partial Claims, Loan Modifications & Selling Your Home)

🏠 Behind on Your Mortgage? Here Are Your Real Options

If you’re struggling to make your mortgage payments, you’re not alone—and more importantly, you’re not out of options.

But here’s the problem…

Most homeowners are given information that’s confusing, overwhelming, or incomplete.

So let’s simplify this the way it actually works.

👉 Everything comes down to one question:

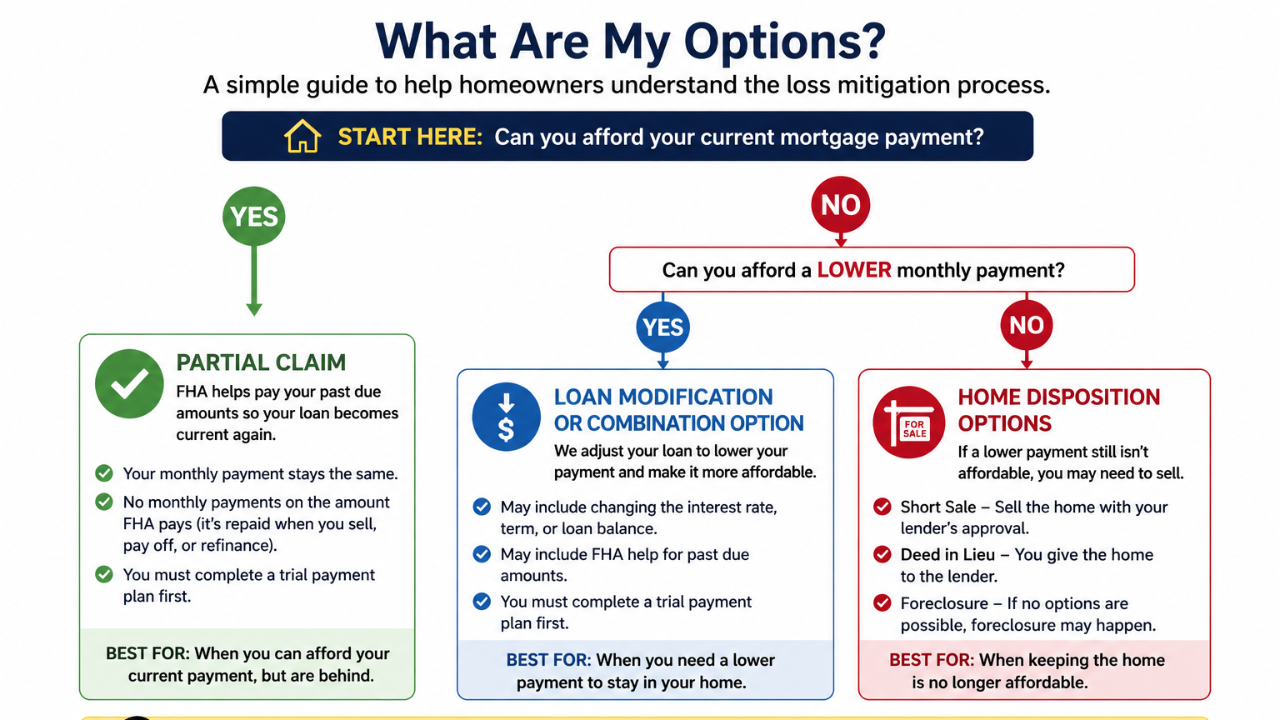

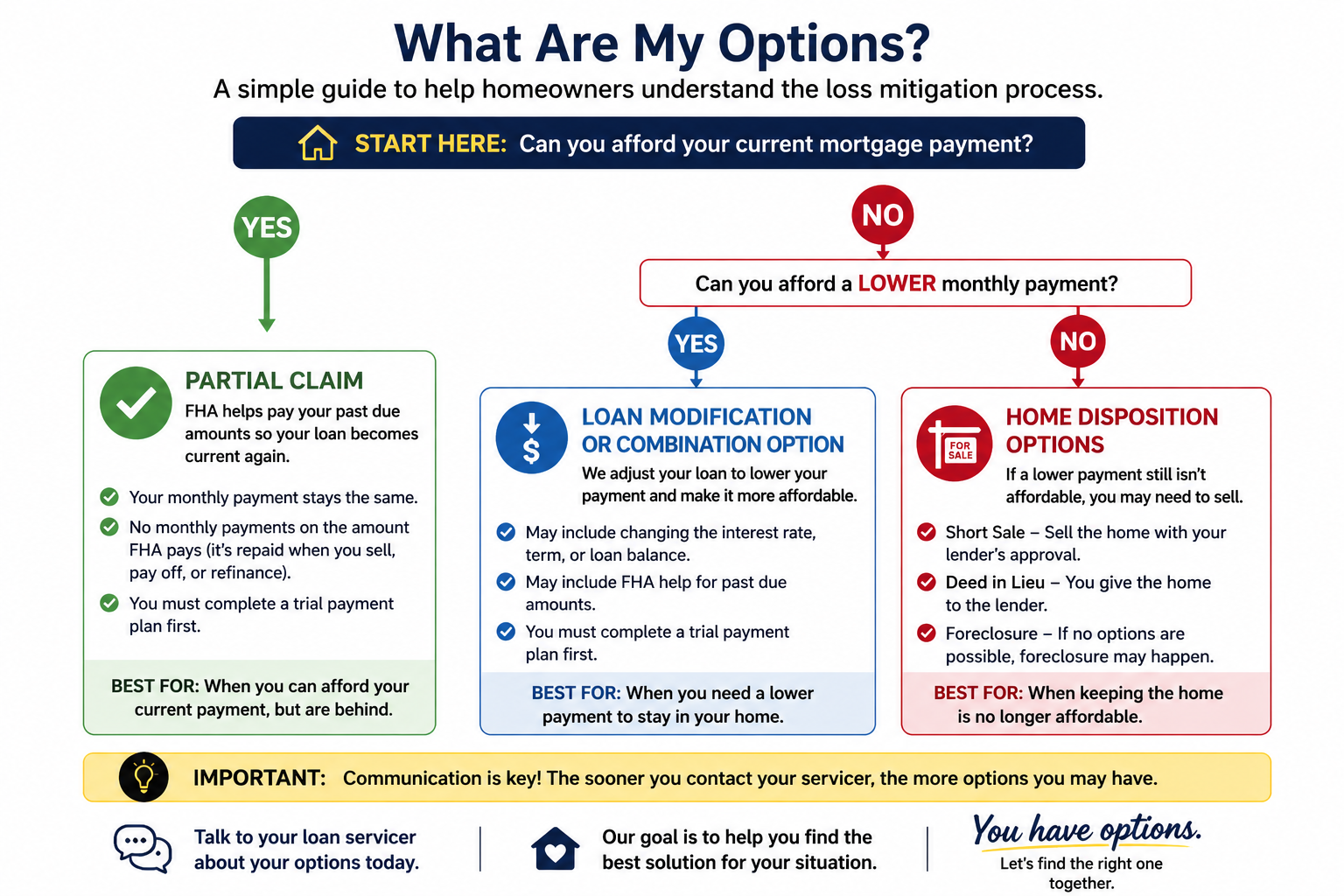

Can you afford your current mortgage payment?

🧭 START HERE: Can You Afford Your Current Payment?

This is the exact decision point lenders use when reviewing your file.

Your answer determines everything that comes next.

✅ If YES — You Can Afford Your Current Payment

👉 Your Best Option: Partial Claim (FHA Loans)

If your income is stable and you can afford your current payment—but you’ve fallen behind—this is often the best-case scenario.

A Partial Claim allows FHA to step in and help bring your loan current.

💡 How It Works:

- FHA pays your past-due balance to your lender

- Your loan becomes current again

- That amount becomes a separate balance (no monthly payments)

- You repay it later when you sell, refinance, or pay off your loan

👍 Why Homeowners Like This Option:

- Your monthly payment stays the same

- You avoid foreclosure

- You don’t need to come up with a large lump sum

👉 Best for: Homeowners who had a temporary setback but are now back on their feet.

❌ If NO — You Cannot Afford Your Current Payment

Now we go one level deeper.

👉 Next question:

Can you afford a LOWER monthly payment?

🔽 If YES — You Can Afford a Lower Payment

👉 Your Best Option: Loan Modification (or Combination Option)

A Loan Modification is designed to make your mortgage more affordable long-term.

Instead of just catching you up, it changes your loan.

💡 How It Works:

- Your interest rate may be lowered

- Your loan term may be extended

- Missed payments may be added to the balance

- In some cases, a Partial Claim is combined with the modification

👍 Why This Works:

- Your monthly payment is reduced

- You stay in your home

- It creates a long-term solution—not just temporary relief

👉 Best for: Homeowners whose income has changed and need a lower payment to stay in the home.

🚨 If NO — You Cannot Afford Even a Lower Payment

This is the hardest conversation—but it’s also where the right strategy can protect you.

👉 Your Best Option: Home Disposition (Selling Strategically)

If the home is no longer affordable, the goal shifts from saving the home to protecting your financial future.

💡 Your Options:

🏡 Sell your home outright if you have equity. Hire a local Realtor.

🏡 Short Sale- This is used only when you owe more on the home than its worth.

- Sell your home for less than what’s owed

- Lender approves the sale

- Often avoids foreclosure

🔑 Deed in Lieu

- You voluntarily transfer the home back to the lender

- Avoids going through foreclosure

⚖️ Foreclosure (Last Resort)

- Happens if no action is taken

- Has the biggest impact on credit and future opportunities

👉 Best for: Homeowners who cannot realistically afford to keep the home.

🔄 Why This Decision Flow Matters

Most homeowners are told about options—but not how to choose between them.

Here’s the simple truth:

- Partial Claim fixes the past (catches you up)

- Loan Modification fixes the future (lowers your payment)

- Selling protects you when staying isn’t possible

👉 The key is choosing the right path early—before your options shrink.

⚠️ Common Mistakes Homeowners Make

- Waiting too long to ask for help

- Thinking forbearance solves the problem

- Not understanding what they can actually afford

- Ignoring communication from their lender

👉 The earlier you act, the more control you have.

💡 Pro Tip: Timing Is Everything

The biggest difference between homeowners who save their home—and those who don’t—is timing.

The sooner you:

- Understand your options

- Review your numbers honestly

- Take action

👉 The better your outcome will be.

❓ Frequently Asked Questions

What is better: Partial Claim or Loan Modification?

It depends. If you can afford your current payment, a Partial Claim is better. If not, a Loan Modification may be needed.

Can I get both a Partial Claim and a Loan Modification?

Yes. In some cases, they are combined to create a more affordable solution.

What if I can’t afford my home anymore?

You may need to look at a short sale or deed in lieu to avoid foreclosure.

Do I have to go into foreclosure?

No. There are multiple options available before foreclosure—but you must act early.

🏁 Final Thoughts

If you’re behind on your mortgage, the most important thing to understand is this:

👉 You have options—but they depend on your situation.

Everything comes back to affordability.

And once you know where you stand, you can make the right move—before it’s too late.

If you’re:

- Behind on payments

- In forbearance

- Or unsure which option is right

👉 Let’s walk through your situation together.

We help homeowners understand their options clearly—so you can make the best decision for your future. Email me: [email protected]

We also educate Realtors and Investors on how to help sellers when they are behind on their mortgage.

Reach out today before your options become limited.

Here is a cheat sheet:

Note: I am not employed or associated with HUD/FHA. Sharing my own opinions based on the public HUD 4000.1 Handbook.

AI helped in creating this post.