FHA Modification Waterfall Explained

May 04, 2026

📝 After Forbearance: What Are Your Mortgage Options? (FHA Modification Waterfall Explained)

🏠 Finished Your Forbearance? Here’s What Happens Next

If you’ve already completed a mortgage forbearance plan, you’re now at one of the most important decision points in the entire process.

This is where many homeowners get stuck.

Because forbearance gave you temporary relief…

but now you need a long-term solution.

👉 And the question your lender is asking right now is simple:

Can you afford your mortgage payment moving forward?

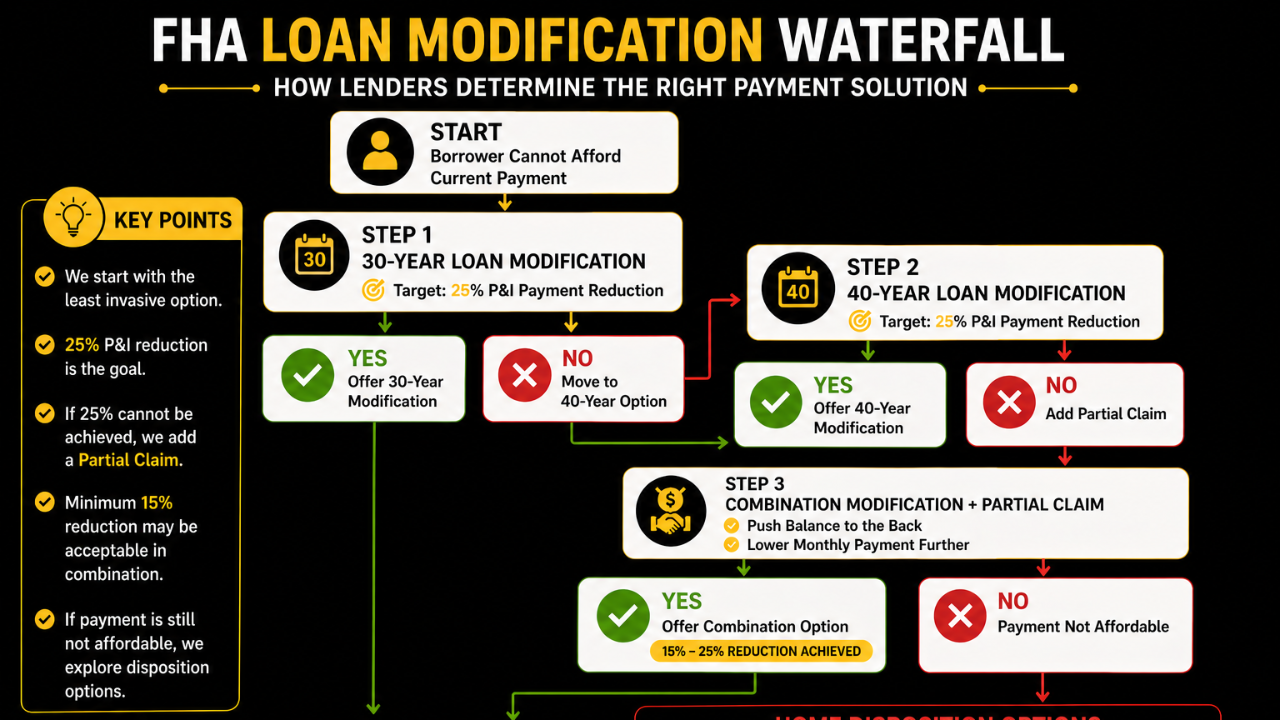

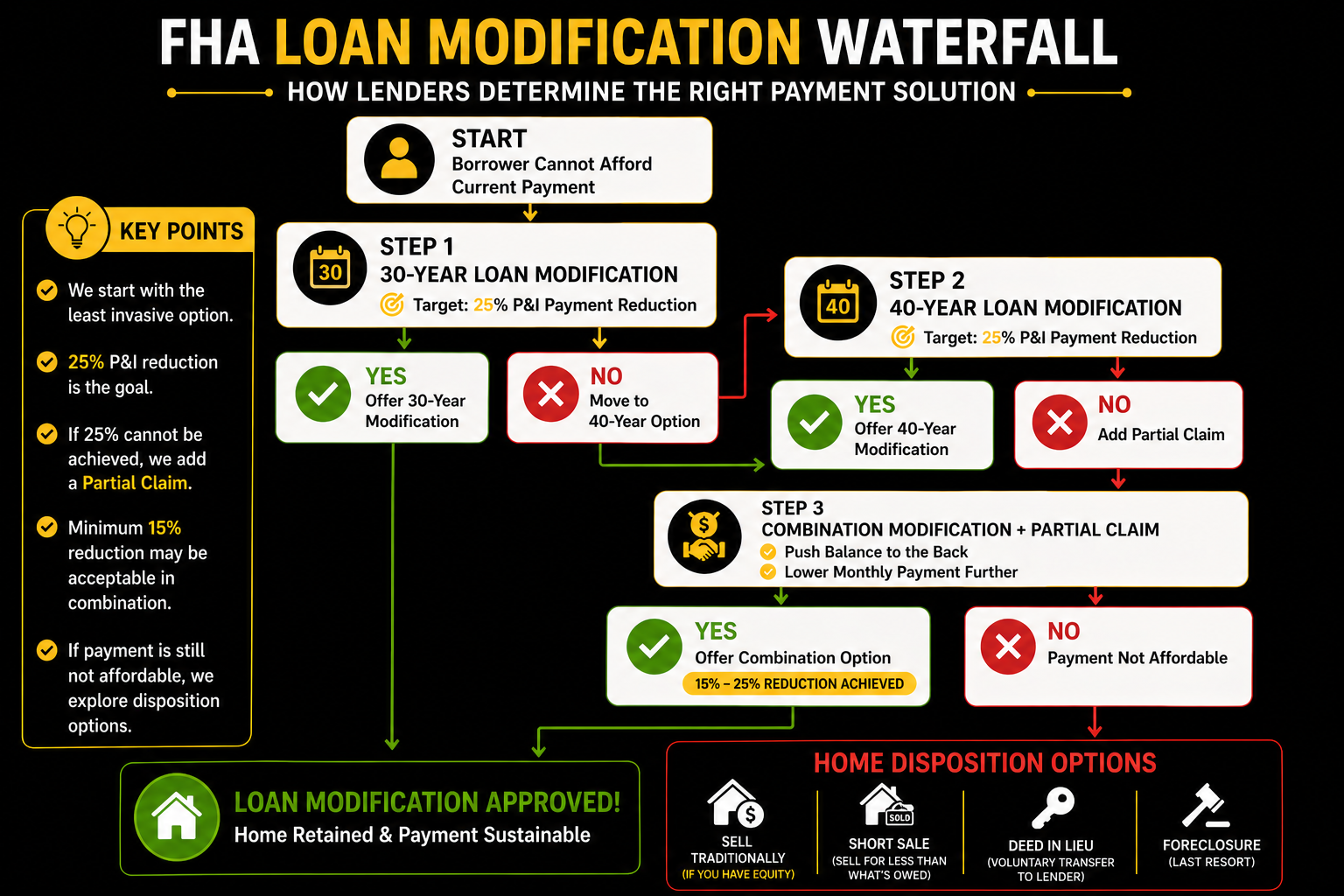

🔄 Understanding the FHA “Waterfall” Process

After forbearance, lenders don’t just guess what option to give you.

They follow a structured system called the FHA Loan Modification Waterfall.

This process is designed to:

- Evaluate your financial situation

- Try to keep you in your home

- Create a payment that is actually affordable

👉 And they must go step-by-step in a specific order.

⚠️ Step 1: You Cannot Afford Your Current Payment

If you’ve reached this stage, it means:

- Your hardship impacted your income

- Your current mortgage payment no longer works

- A simple catch-up option (like a Partial Claim alone) isn’t enough

👉 So now the focus shifts to reducing your payment.

🧭 Step 2: 30-Year Loan Modification

The first option lenders must try is a 30-year loan modification.

💡 What This Means:

- Your loan is restructured

- Missed payments are added into the balance

- The loan is re-amortized over 30 years

- The goal is to reduce your payment

🎯 Target:

👉 25% reduction in your principal and interest payment

If this reduction is achieved:

✔ This is the option offered to you

⏳ Step 3: 40-Year Loan Modification

If a 30-year modification doesn’t reduce your payment enough:

👉 The lender moves to a 40-year loan modification

💡 Why This Helps:

- Extending the loan term lowers your monthly payment

- Gives more flexibility to reach affordability

Again, the goal is:

👉 A 25% payment reduction

If that target is hit:

✔ You’re offered the 40-year modification

💰 Step 4: Combination Option (Modification + Partial Claim)

If the payment still isn’t affordable after extending the term:

👉 FHA allows a Combination Loan Modification + Partial Claim

💡 How This Works:

- Part of your balance is moved to the back of the loan (Partial Claim)

- The remaining balance is modified

- This lowers your payment even further

🎯 Target Range:

- Ideally: 25% reduction

- Acceptable: 15%–25% reduction

✔ If this works → You’re approved for this option

🚨 What If the Payment Still Isn’t Affordable?

This is the hardest—but most important—part to understand.

If after:

- 30-year modification

- 40-year modification

- Combination option

👉 The payment is STILL not affordable…

Then the lender determines:

The home is no longer financially sustainable.

🏡 Final Step: Home Disposition Options

At this stage, the goal shifts from saving the home to protecting your financial future.

Your options may include:

💵 Sell Traditionally (If You Have Equity)

- Sell your home on the market

- Pay off the loan

- Walk away with remaining equity

📉 Short Sale

- Sell for less than what’s owed

- Requires lender approval

- Helps avoid foreclosure

🔑 Deed in Lieu

- Voluntarily transfer the home back to the lender

⚖️ Foreclosure (Last Resort)

- Happens if no action is taken

- Has the biggest long-term impact

🧠 Why This Process Matters

Many homeowners believe they can just “apply for a modification” and get whatever they need.

That’s not how it works.

👉 Lenders must follow a structured system

👉 Each step has rules and targets

👉 Everything is based on affordability

💡 Key Takeaway

- Forbearance = Temporary relief (already completed)

- Modification = Fixes your payment moving forward

- Partial Claim = Helps reduce what you owe upfront

- Selling = Protects you if staying isn’t possible

👉 The goal is always to find a solution you can actually sustain.

⚠️ Common Mistakes After Forbearance

- Waiting too long to respond to your lender

- Assuming you’ll automatically get approved

- Not understanding what payment you can truly afford

- Ignoring letters or deadlines

👉 This is where many homeowners lose options.

📌 Pro Tip: Be Honest About Affordability

The best outcome comes from being honest about your numbers.

Not what you hope you can afford…

👉 But what you can realistically sustain long-term.

❓ FAQs

What happens after mortgage forbearance ends?

You must move into a long-term solution like a loan modification, repayment plan, or selling the home.

Can I get a loan modification after forbearance?

Yes, many homeowners transition directly into a modification after completing forbearance.

What if I still can’t afford my home?

You may need to consider selling options like a short sale or traditional sale if you have equity.

Will I automatically qualify for a modification?

No. You must meet guidelines, and lenders must follow the FHA waterfall process.

🏁 Final Thoughts

If your forbearance has ended, you are now at a critical decision point.

👉 The next step determines whether you:

- Keep your home

- Restructure your loan

- Or move on strategically

The key is understanding your options—and acting early.

If you’ve completed forbearance and:

- Don’t understand your options

- Are being offered a modification

- Or aren’t sure what to do next

👉 Let’s walk through your situation together.

We educate homeowners—before it’s too late.

Reach out today and take control of your next step. [email protected]

Or reach out to a HUD approved Counselor.

Stephanie Parks

Note: I am not employed or associated with FHA/HUD. These are my opnions based off the FHA HUD Handbook that is public knowledge. This is not legal advice and these are my own opinions.

AI helped in the making of this post.