Forbearance Plans: What They Are, How They Work, and What Happens Next (Complete Guide for FHA loan types))

Apr 30, 2026

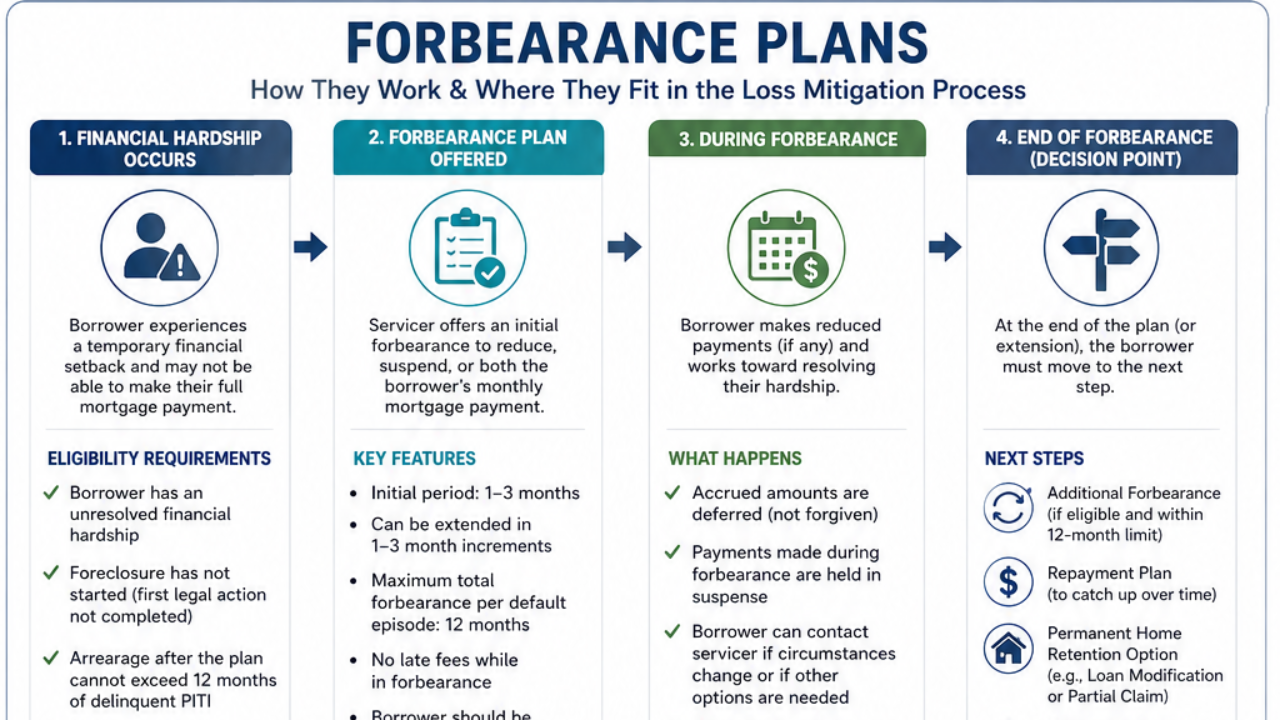

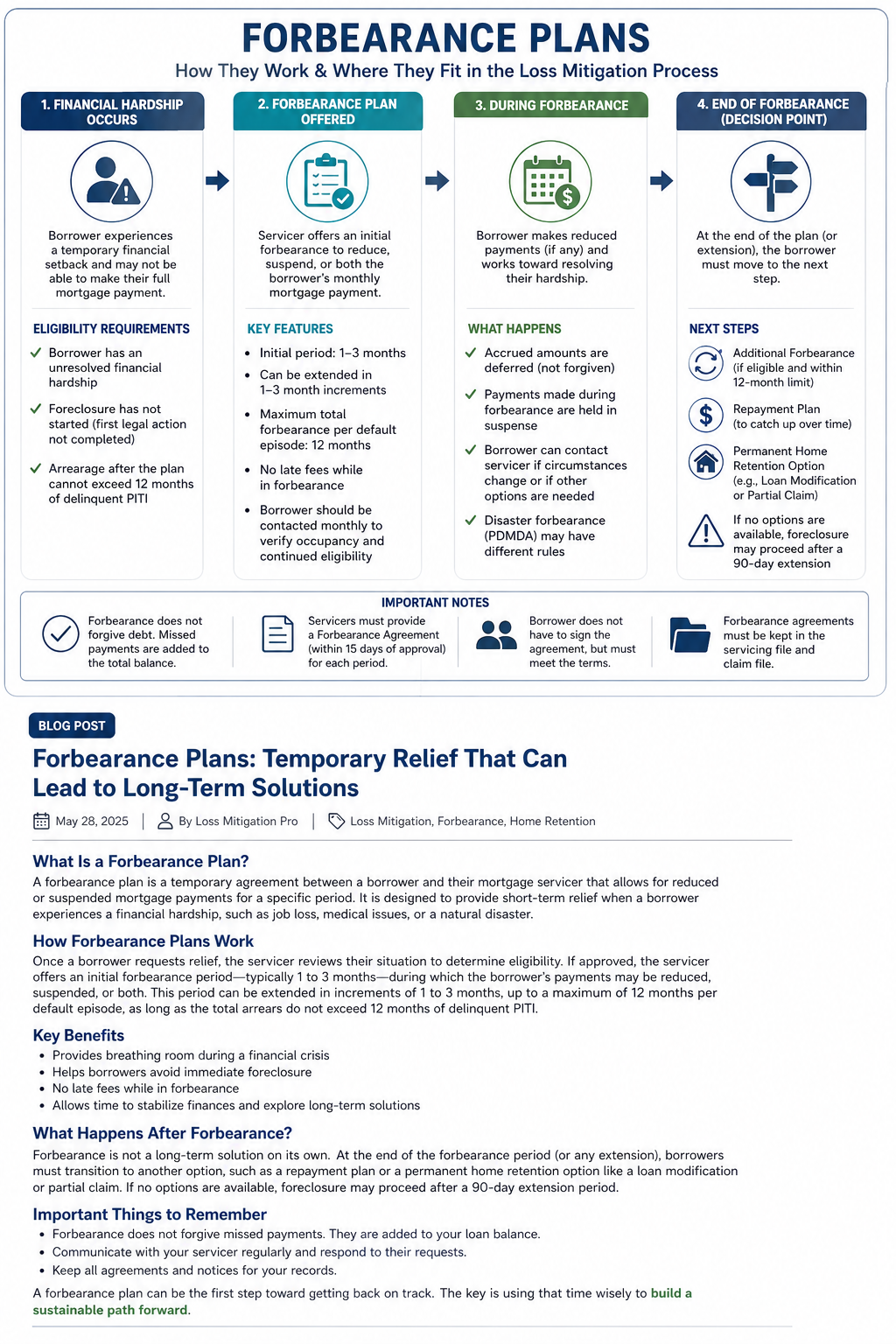

🏠 What Is a Forbearance Plan?

A mortgage forbearance plan is a temporary agreement between a borrower and their mortgage servicer that allows for reduced or suspended mortgage payments during a financial hardship.

It is designed to give homeowners short-term relief, not permanent forgiveness.

👉 The key thing to understand:

Forbearance pauses or reduces payments—but the missed payments are still owed.

⚠️ When Is a Forbearance Plan Used?

Forbearance is typically used when a homeowner is experiencing a temporary financial hardship, such as:

- Job loss or reduction in income

- Medical emergencies

- Divorce or family crisis

- Natural disasters (FEMA-declared areas)

- Temporary business interruption

To qualify, borrowers generally must:

- Confirm they are experiencing a financial hardship

- Not be too far into the foreclosure process

- Stay within allowable delinquency limits (typically not exceeding 12 months of missed payments)

⏳ How Long Does a Forbearance Plan Last?

Most mortgage forbearance plans follow FHA guidelines:

- Initial period: 1 to 3 months

- Extensions: Allowed in 1–3 month increments

- Maximum duration: Up to 12 months per default episode

👉 Servicers must review the borrower monthly to confirm they still qualify.

💡 How Forbearance Payments Work

During a forbearance plan, the mortgage servicer may:

- Reduce the monthly payment

- Suspend the payment entirely

- Or apply a combination of both

Important:

- Late fees are typically waived during the forbearance period

- Any payments made may be placed into a suspense account until they equal a full payment

- The total unpaid amount continues to accumulate as arrears

🚫 Does Forbearance Forgive Mortgage Debt?

No.

This is one of the biggest misconceptions.

👉 Forbearance does NOT erase what is owed.

Instead:

- Missed payments are deferred

- The balance must be addressed later through another solution

🔄 What Happens After a Forbearance Plan Ends?

At the end of a forbearance period, the borrower must transition into a long-term solution.

Common next steps include:

1. Repayment Plan

Catch up on missed payments over time by adding an extra amount to monthly payments.

2. Loan Modification

Permanently adjust loan terms to create a more affordable payment.

3. Partial Claim (FHA Loans)

Move the missed payments to the back of the loan as a separate, interest-free balance.

4. Additional Forbearance

If hardship continues and eligibility remains, the plan may be extended (within limits).

5. Home Disposition Options

If the borrower cannot afford to keep the home:

- Short sale

- Deed in lieu of foreclosure

👉 If no option is approved, foreclosure may resume after a 90-day extension window.

📉 What Causes a Forbearance Plan to Fail?

A forbearance plan may fail if:

- The borrower stops communicating with the servicer

- The property becomes vacant or abandoned

- The borrower does not comply with agreed terms

- The hardship situation is not resolved or worsens

When a forbearance fails:

👉 The servicer must evaluate the borrower for other loss mitigation options.

📊 Key Benefits of a Forbearance Plan

- Provides immediate financial relief

- Helps borrowers avoid foreclosure temporarily

- Gives time to stabilize income

- Allows borrowers to explore long-term solutions

⚠️ Risks and Considerations

- Payments are not forgiven

- Arrears can grow quickly

- Not a long-term solution

- Requires a follow-up plan to resolve the debt

👉 Forbearance is a bridge—not the destination.

📌 Pro Tips for Homeowners

- Stay in constant communication with your servicer

- Understand your next step BEFORE the plan ends

- Keep documentation of all agreements

- Ask about all available options—not just forbearance

🧠 Expert Insight (Use This for Authority Positioning)

Forbearance is often the first step in the loss mitigation process, but it should never be the final plan.

The most successful outcomes happen when borrowers use this time strategically to transition into a sustainable long-term solution, such as a loan modification or partial claim.

Is forbearance a good idea?

Yes, if your hardship is temporary. But it must be followed by a long-term solution.

Will forbearance hurt my credit?

It depends on how the servicer reports it, but missed payments can still impact credit.

Can I extend my forbearance?

Yes, if you still qualify and remain within program limits.

What is better than forbearance?

A permanent solution like a loan modification is better for long-term stability.

🏁 Final Thoughts

A mortgage forbearance plan can be a powerful tool during financial hardship—but only if it’s used correctly.

👉 It buys time.

👉 It creates breathing room.

👉 But it requires a plan for what comes next.

If you’re navigating a forbearance or helping clients through one, understanding the full process is the difference between temporary relief and long-term success.

Are you a Real Estate Agent or Investor and want to learn more about options for homeowners? Join me in my short sale course. Get an education to help sellers the right way.

- mortgage forbearance plan

- FHA forbearance guidelines

- what is forbearance mortgage

- how does forbearance work

- mortgage payment relief options

- loss mitigation options FHA

- what happens after forbearance

Stephanie Parks

AI assisted in creating this post.

Note: I am not employed or associated with FHA/HUD. This is from my own research from the public HUD handbook 4000.1

This course is for educational purposes only. I am not providing legal advice, and I am not associated with a government agency. The information shared is based on my own experience, research, and opinions. Always consult the appropriate legal, compliance, or licensed professionals when needed.